Hawaii

| Hawaii owes more than it owns. |

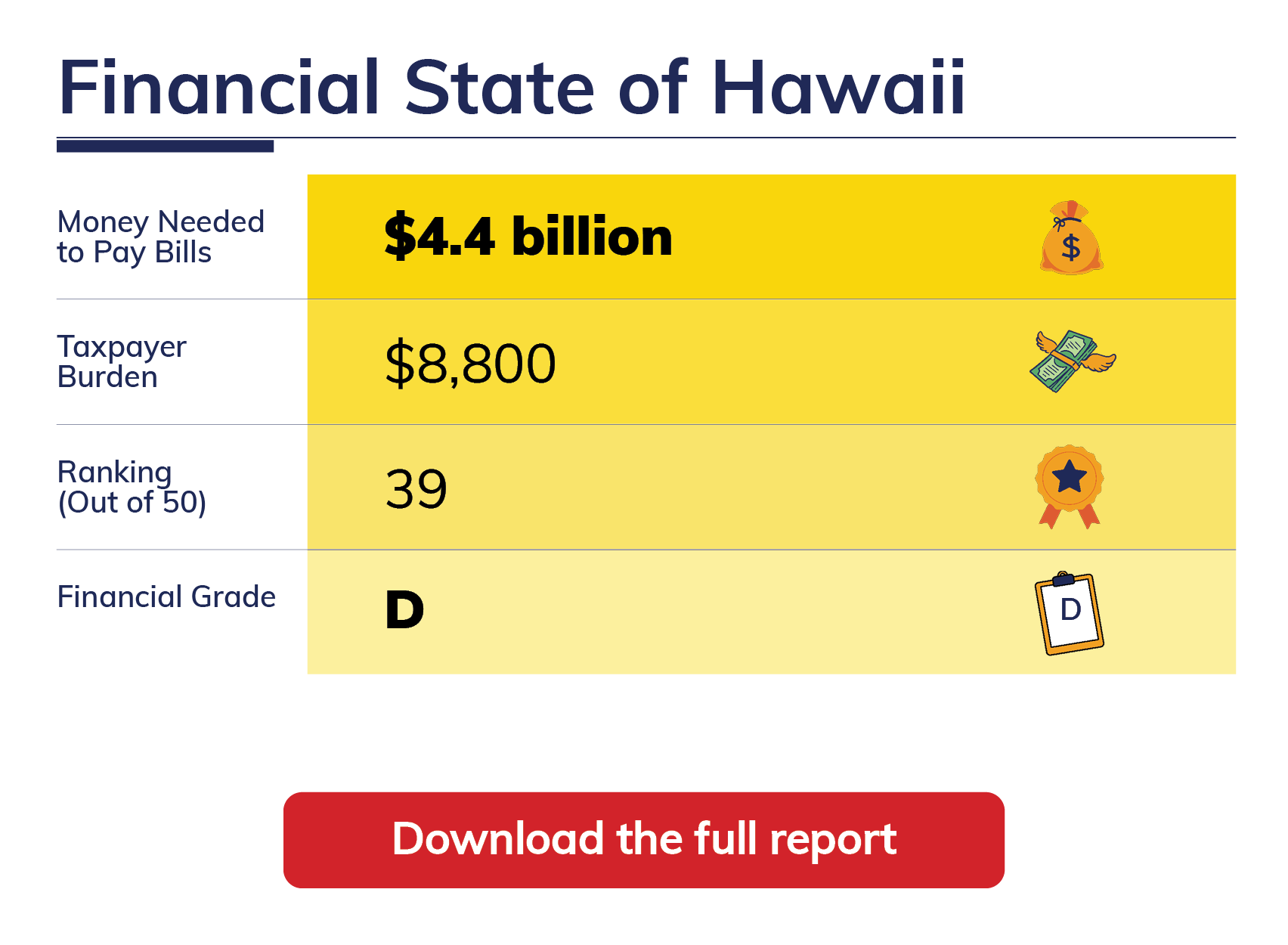

| Hawaii has a -$8,800 Taxpayer Burden.™ |

| Hawaii is a Sinkhole State without enough assets to cover its debt. |

| Elected officials have created a Taxpayer Burden™, which is each taxpayer's share of state bills after its available assets have been tapped. |

| TIA's Taxpayer Burden™ measurement incorporates both assets and liabilities, not just pension debt. |

| Hawaii only has $17.3 billion of assets available to pay bills totaling $21.7 billion. |

| Because Hawaii doesn't have enough money to pay its bills, it has a -$4.4 billion financial hole. To fill it, each Hawaii taxpayer would have to send -$8,800 to the state. |

| Hawaii's reported net position is overstated by $578.2 million, largely because the state delays recognizing losses incurred when the net pension liability increases. |

| The state's financial report was released 214 days after its fiscal year end, which is considered untimely according to the 180 day standard. |

Prior Years' TIA Reports

2023 Financial State of Hawaii

2022 Financial State of Hawaii

2021 Financial State of Hawaii

2020 Financial State of Hawaii

2019 Financial State of Hawaii

2018 Financial State of Hawaii

2017 Financial State of Hawaii

2016 Financial State of Hawaii

2015 Financial State of Hawaii

2014 Financial State of Hawaii

2013 Financial State of Hawaii

2012 Financial State of Hawaii

2011 Financial State of Hawaii

City and Municipal Reports

Other Resources

Hawaii Annual Comprehensive Financial Reports

Publishing Entity: Department of Accounting and General Services